Credit card debt is one of the most common—and expensive—financial burdens many people carry. In the U.S., total revolving debt (which includes credit card balances) recently surpassed $1.18 trillion. Meanwhile, the average credit card interest rate is hovering in the low 20s (about 22-22.5%) for accounts that carry a balance. If you’re feeling overwhelmed by credit card bills, you’re not alone—and there are effective strategies you can use to get out of debt faster and start redirecting those payments toward something more positive.

This guide lays out 10 smart, actionable strategies to accelerate your credit card payoff. Use the ones that best match your personality, financial situation, and comfort level. You don’t have to do all of them, but combining a few will exponentially speed up your progress.

1. Face the Numbers & Create a Clear Snapshot

Before you can make real progress, you need a full, honest inventory of what you owe and what you’re paying.

- List every credit card: include current balance, interest rate (APR), minimum payment, due date, and whether there are fees or promotional rates.

- Calculate total interest cost: take each card’s balance × APR to estimate roughly how much interest you’re paying per year (or per month). This helps you see how much debt is “working” against you.

- Track income & expenses: build or revise your budget—know how much comes in, how much goes out, and where there may be slack (or unnecessary spending).

By grounding yourself in the reality of your debt load—interest, minimums, payment dates—you build the control that leads to faster payoff. Clarity also helps motivate: seeing that high-APR card costing hundreds every month can be a strong incentive to take action.

👉 If seeing your debt and expenses feels overwhelming, don’t worry—you don’t have to figure it out alone. Our beginner-friendly budgeting guide breaks it down: Budgeting for Beginners: 7 Easy Steps to Take Control of Your Money

2. Pay More Than the Minimum Whenever Possible

Minimum payments are designed to keep you “current” but not to get you out of debt quickly. Paying only minimums is often a recipe for slow progress and heavy interest charges.

- Even adding just a bit more each month (e.g. 5–20% above the minimum) sends more to principal. Over time that makes a substantial difference.

- If you can, pay off the full statement balance each month to avoid interest altogether—but of course, that’s not always possible.

Statistically, many U.S. consumers carry balances for years—because they only pay minimums. According to a 2025 Bankrate report, about 60% of credit card debtors have carried a balance for at least a year. If you consistently pay above the minimum, you avoid that multi-year drag.

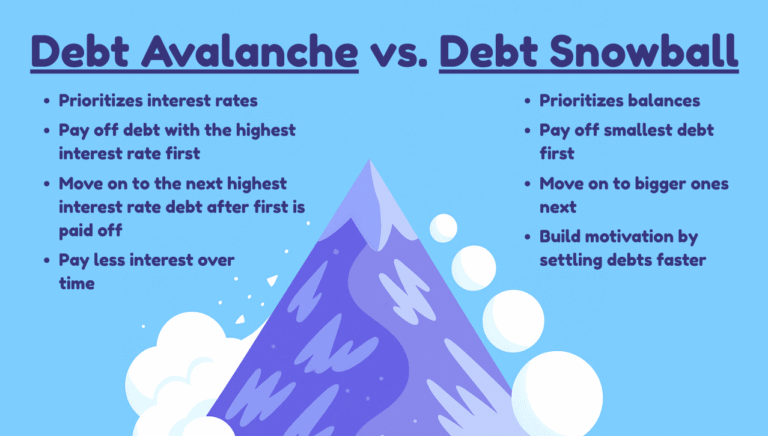

3. Use a Strategic Payoff Method: Avalanche vs. Snowball

Two of the most popular methods for tackling multiple balances are the avalanche method and the snowball method. Each has trade-offs, so choosing one that aligns with your mindset and financial triggers is key.

- Avalanche method: Focus extra payments on the card with the highest interest rate first, while paying minimums on the rest. Once that one is paid off, roll those payments into the next highest rate. Benefit: you pay less interest over time.

- Snowball method: Focus extra payments on the card with the lowest balance first. Once that’s gone, you move on to the next smallest, etc. Benefit: you get “quick wins” which boost motivation.

If you’re more motivated by psychological rewards (seeing debts disappear faster), the snowball may keep you going. If you’re comfortable delaying payoff of your highest-interest card for a bit longer in order to save more overall, the avalanche method is statistically more efficient.

4. Consolidate Your Debt Where It Helps

If you have multiple credit cards with different APRs, consolidating can simplify payments and reduce interest—but done carefully.

- Balance transfer credit cards: These often offer a 0% or very low intro APR on transferred balances for a period (6-21 months or more). If you can pay off during that period and avoid hefty transfer fees, this can save a lot.

- Personal consolidation loans: Instead of keeping many revolving balances, you replace them with a fixed payment, often at a lower interest rate. The steady schedule helps you plan.

However, watch out for pitfalls: fees, expiring promo rates, high rate after intro period, and the temptation to use paid-off cards again.

5. Negotiate Interest Rates or Seek Hardship Programs

Many people don’t realize how much negotiating or leveraging card issuer programs can help.

- Call your credit card issuer: If you have a solid on-time payment history, you can often negotiate a lower interest rate. Even a small reduction (e.g. 3-5%) can save hundreds (or more) over time.

- Hardship programs: If you’re experiencing a job loss, medical bills, or other financial stress, many issuers offer temporary relief—lowered interest, waived fees, reduced payment. Using these can stop debt from spiraling.

- Credit counseling agencies: Nonprofits in many states will help you set up a repayment plan, sometimes combining creditor negotiation with budget help. It can lower costs of repayment and provide structure.

These options can reduce the interest burden so more of what you pay goes toward reducing principal, not just fees and interest.

6. Trim Unnecessary Spending and Redirect That Cash

Payoff speed often comes down to freeing up extra dollars. Even small cuts across the board add up.

- Audit your recurring expenses (subscriptions, memberships, streaming services, etc.). Cancel or downgrade what you don’t need or use frequently.

- Watch non-essential discretionary spending: eating out, impulse buying, frequent upgrades. Those smaller, habitual things often consume surprisingly large shares of your budget.

- Reallocate bonuses, tax refunds, side gig income, or money from gifts toward debt payoff. If you see an extra chunk of cash, using it toward outstanding balances can pull your debt timeline forward significantly.

For example: Suppose you pay $100/month toward groceries, but you find that with meal-planning & bulk purchases you can cut that to $80. That $20 saved can go directly to your credit card with the highest APR, and over a year that’s $240 plus interest you’d otherwise be paying on it.

💡 Cutting expenses doesn’t have to feel like sacrifice. For dozens of creative ideas to save money while still enjoying life, see our guide: 75 Frugal Living Tips That Actually Work.

7. Automate Payments, Save Penalties & Protect Your Score

Missed payments trigger late fees, penalty APRs, and can damage credit scores—making your debt costlier in both money and opportunity.

- Set up automatic payments for at least the minimum due on each card so you never miss a due date.

- If possible, schedule extra payments (from your bank account) for your target card (avalanche or snowball) to hit right after payday, when you know funds are available.

- Monitor credit card accounts regularly to ensure charges are accurate, fees aren’t being added without notice, and you understand when intro-rates or promotional periods expire.

Statistics show that penalty APRs can reach very high rates when payments are late, so avoiding late payments is not just about credit—it’s about saving money.

8. Make Use of Windfalls & Extra Income

Extra income is one of the fastest ways to accelerate payoff—but it often requires deliberately channeling it.

- Use tax refunds, bonuses, monetary gifts, or side-hustle income to make lump-sum payments. Even a single extra large payment can knock down the principal and reduce future interest.

- Consider temporary part-time or freelance work, gig-economy opportunities, or other side income that can be dedicated entirely to debt. If you can, put that money in a separate account so you don’t spend it before it’s deployed.

- Sell things you don’t need: declutter, hold a garage sale, or use online marketplaces. The proceeds may seem small, but applied directly to your balances, they remove debt rather than fund more consumption.

Every bit of extra cash applied to principal (rather than just interest or minimums) compounds in benefit.

9. Monitor Progress and Adjust As Needed; Celebrate Milestones

Debt payoff is a long game; keeping momentum and morale high is often the difference between giving up and getting free.

- Track your balances over time (monthly or every few weeks). Note how much interest you’re paying, how much principal you’re reducing, how the payoff date is moving. Visual charts or debt payoff apps can help.

- Adjust your plan if life changes: income drops or increases, a major expense arises, interest rates change, etc. Flexibility is key. If you find one repayment strategy isn’t inspiring or working, it’s okay to switch (e.g. move from snowball to avalanche or vice versa).

- Celebrate when you pay off a card. When you eliminate one balance, mentally reward yourself (in cost-effective ways). Small wins make a big difference for staying motivated.

By treating each milestone as proof of progress, you’ll build momentum to keep going until every balance is gone. Even paying off one card can feel like a huge weight lifted—and that feeling keeps you moving forward.

10. Protect Your Future: Avoid Repeating the Cycle

Finally, getting out of credit card debt is huge—but staying free of it (or preventing it from ballooning) matters just as much.

- Build an emergency fund. Even a modest cushion ($500-$1,000 or more depending on your situation) can prevent you from relying on credit when unexpected costs hit.

- Improve financial literacy: read, take courses, find mentors or advisors. Understanding interest, credit scores, fees, compounding, and smart borrowing helps you make better choices.

- Use credit cards wisely: charge only what you can pay off, avoid “interest traps” (like owing at high APRs or making purchases when you can’t repay), and pay in full whenever possible.

- Review your credit card terms every year: keep an eye on APR changes, fees, reward program changes. If you find better cards (lower APR, good rewards, no fees), consider switching—but always consider the costs and impacts.

Remember, paying off debt isn’t the finish line—it’s the foundation for a stronger financial future. Protecting yourself with better habits and safety nets ensures you won’t slip back into the same cycle again.

Why These Strategies Work Together

You may wonder: is it better to pick just one or try several? The truth is that using multiple strategies together often accelerates results far more than any single tactic alone.

For example:

- Combining trimming spending + applying windfalls + using the avalanche method can reduce payoff time by months or even years.

- Consolidating debt lowers your interest rate, so more of your payment goes toward principal, while automated payments help ensure consistency.

- Celebrating milestones keeps motivation alive, which helps you stick with the plan instead of getting discouraged.

Moreover, recent data shows that nearly half (46%) of American credit cardholders still carry credit card balances as of mid-2025 (bankrate.com). Among those who carry balances, many delay other financial milestones (saving, investing, big purchases) because of their debt burden. Taking control now doesn’t just reduce what you owe—it frees up options for years to come.

Realistic Timeline & What You Might See

Just so you have expectations:

- If you owe, say, $5,000 across two cards at average APR (~22%), making just minimum payments might stretch repayment over many years and cost thousands of dollars in interest.

- If instead you pay an extra $100-$200/month toward the highest APR card (using avalanche) while keeping up minimums on the rest, you might cut that timeline significantly—possibly 12-24 months shorter, depending on your income, fees, etc.

- Using a balance transfer with 0% intro rate (if eligible) could give you breathing room of 6-18 months to focus on principal—if you resist adding new debt.

Some people get completely out of credit card debt in under a year with aggressive use of windfalls + cutting expenses + using consolidation, while for others it may take 2-3 years. The important part is that you’re making progress and not stuck in neutral.

Takeaways & First Steps

Here are simple, doable next steps to put you on the fast track:

- Gather all credit card statements and list balances, APRs, and minimums.

- Decide if avalanche or snowball fits your personality.

- Identify one or two nonessential expenses you can cut immediately and redirect that money to debt.

- Set up automatic payments.

- If you get a bonus, refund, or extra income, earmark it for debt payoff.

Final Thoughts – You Can Be Free From Credit Card Debt

Paying off credit card debt isn’t easy, but it’s absolutely possible with the right mix of strategy, persistence, and mindset. Whether you use the avalanche or snowball method, negotiate lower interest rates, cut back on spending, or find ways to boost your income, every step moves you closer to freedom.

The key is consistency. Debt payoff doesn’t happen overnight, but with a structured plan, a focus on progress, and the willingness to adjust as life changes, you can steadily chip away at balances. Celebrate your milestones along the way and remind yourself that every payment made is money you’ll never owe again.

Most importantly, once you’ve crushed your debt, protect your future by avoiding the same traps. Build an emergency fund, use credit wisely, and keep learning about personal finance. That way, instead of funneling money toward interest, you can redirect it toward savings, investments, and the life you truly want.

Be patient, stay motivated, and trust the process—your future debt-free self will thank you.

Frequently Asked Questions (FAQ)

1: How long does it typically take to pay off credit card debt?

It depends on your total balance, interest rates, and how much extra you can pay each month. Some people pay off moderate balances in under a year with aggressive strategies, while others may take 2–3 years. The important thing is consistent progress.

2: Should I use the avalanche method or the snowball method?

Both work—it depends on what motivates you. The avalanche method saves the most money on interest by tackling high APR balances first. The snowball method gives psychological wins by paying off smaller balances first, which can help you stay motivated.

3: Is debt consolidation a good idea?

Consolidation can be useful if it lowers your interest rate or simplifies payments, but be careful of balance transfer fees, expiring promotional rates, or the temptation to rack up new debt on paid-off cards.

4: How can I make extra payments if my budget is tight?

Small, incremental contributions matter. Even redirecting money from cut subscriptions, windfalls like tax refunds or bonuses, or extra side income toward debt can speed up payoff over time.

5: Will paying off credit card debt improve my credit score?

Yes. Reducing balances and paying on time can improve your credit utilization ratio and payment history, both of which are key factors in your credit score. However, score improvements may take a few months to fully reflect.

6: What if I can’t pay more than the minimum?

Start where you can. Even making minimum payments consistently avoids late fees and penalty APRs. Once you free up extra money, channel it toward your highest-interest debt to accelerate payoff.

7: How can I prevent falling back into debt?

Build an emergency fund, use credit cards responsibly (pay in full whenever possible), monitor spending habits, and continue educating yourself about personal finance. Planning ahead is the best way to stay debt-free.

[…] score back? The quickest way to lower credit utilization is to pay off debt strategically. Our post 10 Smart Strategies to Pay Off Credit Card Debt Faster walks you through simple, proven methods to cut balances and see results […]

I paid off my credit card using the above listed strategies and talk about the feeling of FREEDOM!

That’s amazing. Nothing beats the feeling of finally being debt-free!

Good advice!

Thank you!

[…] Ready to crush your credit cards even faster? Head over to 10 Smart Strategies to Pay Off Credit Card Debt Faster for proven tips you can start using […]

[…] card debt is your biggest hurdle, don’t worry — we’ve got you covered. Read our post on 10 Smart Strategies to Pay Off Credit Card Debt Faster for practical tips you can use right […]

[…] If credit card balances are holding you back, check out our guide: 10 Smart Strategies to Pay Off Credit Card Debt Faster for practical tips to speed up the […]